When is a tax rise not a tax rise?

Fiscal drag.

If you’re not familiar with this rather uninspiring economic term, fiscal drag is what happens when wages go up, but tax thresholds stay fixed. The result is some taxpayers are pushed into a higher tax bracket.

Put even simpler, it’s often described as a ‘stealth tax’.

By freezing thresholds, the government gets to increase tax receipts, without actually having to say it’s putting up taxes.

This has been the case with UK income tax since 2021, when the previous government froze personal income tax thresholds. Last Autumn, Rachel Reeves confirmed this freeze would end and thresholds will once again rise with inflation each year. However, this won’t happen till 2028.

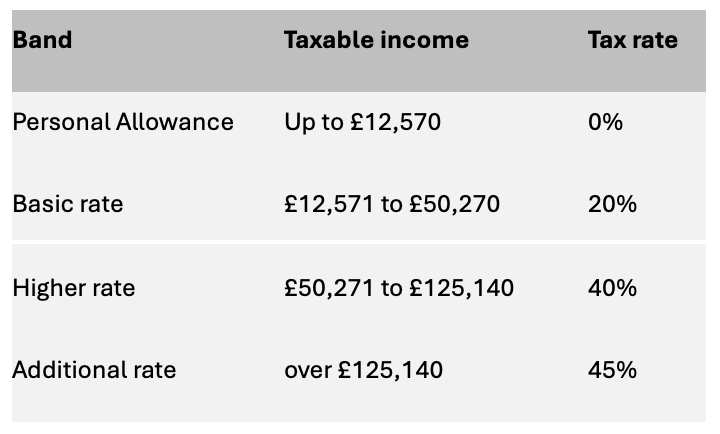

Current UK tax bands

Why is fiscal drag such a big deal right now?

Tax thresholds haven’t changed to reflect some of the periods of record wage growth in the last few years. As a result, millions of taxpayers’ bills are going to be affected by fiscal drag.

In 2027/28, the last financial year before the freeze is lifted, there will be 4.2 million more people paying income tax, and another 4.1 million in the higher-rate or additional-rate bracket, according to projections from the Office for Budget Responsibility. That’s because there’s a large and growing gap between income tax thresholds and what they would have been if they’d followed inflation. In that same year, the personal allowance threshold will be £12,570, nearly £4,000 less than the inflation-linked figure. The higher rate starts at £50,271, which is around £15,000 less than the inflation-linked figure.

(In Scotland, where there are a larger number of tax thresholds, the situation is slightly different, only higher, advanced and top rate thresholds have been frozen for the 2025/26 financial year, the starter, basic and intermediate rates have risen above inflation.)

Threshold freezes are creating additional taxpayers

Caution: tax traps ahead

This isn’t the only way your tax bill could change without you really noticing. There are two so-called ‘tax traps’ that can catch taxpayers out.

The personal allowance taper

If you earn between £100,000 and £125,140, your personal allowance is progressively removed (or tapered). For every £2 earned above £100,000, you lose £1 of your allowance. Above the top rate, you lose all your personal allowance. This is sometimes referred to as the ‘60% tax rate’, as for every £100 of income you pay £40 in income tax and lose another £20 from tapering.

Removing child benefits

Child benefit entitlement is also tapered for higher earners. For every £200 earned over £60,000, you must repay 1%. Once you reach the £80,000 you have to repay all your child benefit received. Tax-free childcare and some free childcare hours also disappear for those earning more than £100,000.

It’s worth noting that the High Income Child Benefit charge is based on individual income – two parents earning £59,000 can still access their full child benefit entitlement.

What can you do to prepare?

While these warnings might sound overly negative, with a good amount of planning it’s possible to reduce some of the impact.

Increase your pension payments

The most straightforward way to avoiding these tax traps is by upping your pension contributions. This allows you to lower your adjusted net income. For example, if you’re earning more than £100,000 and at risk of losing your personal allowance, increasing your pension payments could bring you back below the threshold.

You may be able to pay in up to £60,000 per year into a pension scheme without paying income tax. However, your annual allowance is also tapered if you’re a higher earner, reducing by £1 for every £2 you earn over £260,000. (You’ll need to declare tax relief on your pension contributions using a self-assessment tax return).

Salary sacrifice

As well as paying directly into your pension, an element of salary sacrifice – for example, a Cycle to Work scheme, or buying an electric vehicle through your employer – can help make your income more tax-efficient. These can potentially not only reduce your taxable income but lower your National Insurance contributions too.

Use your ISA

When trying to stay tax efficient, it’s important to use all available allowances. This includes your annual ISA allowance of £20,000. These have no tax on interest, dividends, or capital gains.

But remember … take advice

Even if the fiscal drag doesn’t push your salary into a higher tax band, or you’re not affected by the 60% tax trap, you might still get caught out by some of the fine print on tax regulations – especially as your income rises. The benefit of taking professional advice is you don’t have to do it alone.

Speak to us about how we can help keep you tax efficient.

The value of your investments, pensions and the income from them can fluctuate (this may partially be the result of exchange rate fluctuations) and you may get back less than the amount invested.

Past performance is not a guide to future performance

The information in this blog was correct as of 30 April 2025.